Understanding Health Insurance: A Guide to Billing and Reimbursement

Navigating the complexities of healthcare finances requires understanding how billing works, and reimbursement is processed, especially with multiple policies becoming common today.

What is Health Insurance?

Health insurance is a contract that helps cover the cost of medical services. It provides financial protection against unexpected healthcare expenses, mitigating potentially devastating bills. Many individuals now find themselves covered by more than one plan – a combination of employer-sponsored and personal policies, or even dual individual plans – seeking broader coverage.

Essentially, you pay a regular premium, and in return, your insurance company agrees to pay a portion of your medical bills. However, the “true test” of health insurance isn’t the initial purchase, but rather how effectively it functions when you actually need care. Understanding this fundamental relationship is crucial for navigating the healthcare system effectively and responsibly.

Types of Health Insurance Plans

A variety of health insurance plans exist, each with distinct features impacting cost and access to care. These plans cater to diverse needs and preferences, but understanding their differences is vital. Common types include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Exclusive Provider Organizations (EPOs), and Point of Service (POS) plans.

The choice depends on factors like desired flexibility, network preferences, and budget. Rising premiums and increasing out-of-pocket costs are prompting many to re-evaluate their options, exploring alternatives to traditional employer-funded plans. New coverage options are emerging to address these financial burdens and improve accessibility.

HMO (Health Maintenance Organization)

HMO plans generally require selecting a primary care physician (PCP) who coordinates all healthcare services. Referrals are typically needed to see specialists within the network, emphasizing managed care and cost control. HMOs often feature lower premiums and out-of-pocket expenses compared to other plan types, but offer less flexibility in choosing providers.

This structure prioritizes preventative care and coordinated treatment. However, accessing care outside the network is usually limited, potentially leading to higher costs. As healthcare costs rise, understanding network restrictions and referral requirements within an HMO is crucial for effective financial planning and access to needed medical services.

PPO (Preferred Provider Organization)

PPO plans offer greater flexibility than HMOs, allowing members to see specialists without a referral. While utilizing in-network providers results in lower costs, PPOs also provide coverage for out-of-network care, albeit at a higher expense. This flexibility comes with typically higher premiums and deductibles compared to HMO plans.

PPOs balance cost and choice, appealing to individuals who value provider selection. Understanding the allowed amount for out-of-network services is vital, as patients are responsible for the difference between the billed charge and the insurance-approved rate. Careful consideration of premium costs versus potential out-of-pocket expenses is key when choosing a PPO.

EPO (Exclusive Provider Organization)

EPO plans represent a middle ground between HMOs and PPOs, typically requiring members to stay within a network of providers for coverage, excluding emergency care. Unlike HMOs, EPOs generally don’t necessitate a primary care physician referral to see specialists, offering more direct access to specialized care.

However, out-of-network care is usually not covered, except in emergency situations, making network selection crucial. EPOs often feature moderate premiums and deductibles. Policyholders should diligently verify provider network participation before seeking treatment to avoid unexpected out-of-pocket costs, as disputes between hospitals and insurers are frequent.

POS (Point of Service)

POS plans blend features of both HMOs and PPOs, offering flexibility but also requiring careful navigation of in-network versus out-of-network costs. Typically, members choose a primary care physician (PCP) who coordinates their care and provides referrals to specialists within the network.

Seeing out-of-network providers is usually possible, but at a higher cost, often involving higher deductibles, coinsurance, and claim submission responsibilities. POS plans aim to balance cost control with member choice, but understanding the referral requirements and cost-sharing differences is vital to avoid unexpected bills, especially given rising healthcare costs and frequent insurer disputes.

Key Health Insurance Terms

Understanding core terminology is crucial for navigating health insurance effectively, especially as costs continue to rise and plans become more complex. The premium is the monthly payment for coverage, while the deductible is the amount you pay before insurance starts covering costs.

A copayment is a fixed fee for specific services, like a doctor’s visit, and coinsurance is a percentage of the cost you share with the insurer after meeting your deductible. Keeping detailed records of all medical expenses and receipts is essential, given potential tussles between hospitals and insurance providers, ensuring accurate claim submissions and dispute resolution.

Premium

The health insurance premium represents the monthly cost of maintaining your coverage, regardless of whether you utilize healthcare services during that period. It’s a recurring expense, similar to a subscription, ensuring access to a network of providers and financial protection against unexpected medical bills.

Rising premiums are a significant concern for many, prompting exploration of alternative coverage options like Health Reimbursement Arrangements (HRAs). Employer-funded HRAs offer a new approach to managing healthcare expenses, and understanding your premium’s value within the broader context of your plan is vital for informed decision-making, especially with increasing out-of-pocket costs.

Deductible

Your health insurance deductible is the amount you pay out-of-pocket for covered healthcare services before your insurance plan begins to pay. It’s a crucial element impacting your overall healthcare costs, often resetting annually. Higher deductibles typically correlate with lower monthly premiums, and vice versa – a trade-off to consider.

Frequent disputes between hospitals and insurers highlight the importance of understanding your deductible and potential out-of-pocket expenses. Careful record-keeping of all medical bills and receipts is essential, particularly as rising healthcare costs continue to challenge many health plans and individuals seeking affordable care.

Copayment

A copayment, often simply called a “copay,” is a fixed amount you pay for a covered healthcare service, typically at the time of service. This applies to doctor visits, specialist appointments, or prescription medications. Copays are usually a flat fee, like $20 for a primary care visit, and don’t count towards your deductible.

Understanding your copay amounts is vital for budgeting healthcare expenses. As employer health insurance struggles to adequately cover costs, knowing these fixed fees helps manage financial burdens. Maintaining detailed records of payments, alongside hospital documents and receipts, is crucial when navigating potential billing issues and ensuring accurate reimbursement.

Coinsurance

Coinsurance represents your share of the costs of a covered healthcare service after you’ve met your deductible. It’s expressed as a percentage – for example, 20% – meaning your insurance pays 80% and you pay the remaining 20% of the allowed amount for that service.

Rising healthcare costs and premiums are pushing individuals to seek multiple insurance policies, and understanding coinsurance is key to managing out-of-pocket expenses. Accurate record-keeping of all medical bills and receipts is essential, especially given frequent disputes between hospitals and insurers. Knowing your coinsurance percentage helps anticipate costs and budget effectively, particularly as traditional employer plans struggle to keep pace with rising expenses.

The Health Insurance Billing Process

The health insurance billing process begins with a healthcare provider submitting a claim to your insurance company for services rendered. This claim includes detailed information about the services, diagnoses, and associated costs.

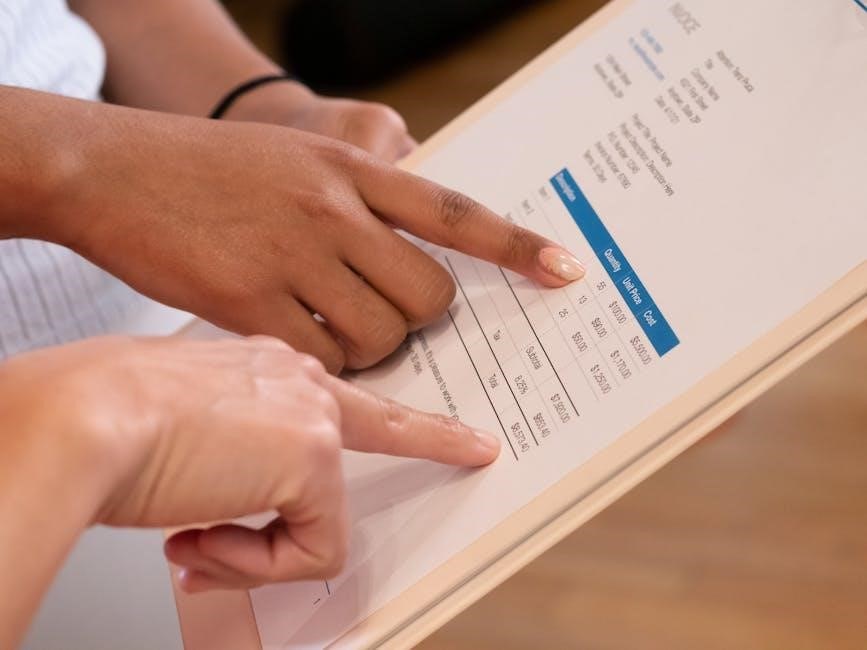

Following claim submission, you’ll receive an Explanation of Benefits (EOB), outlining how your claim was processed – what the provider charged, the amount approved, your coinsurance or copay, and any remaining balance; Accurate medical coding (ICD-10 and CPT) is crucial for proper claim processing. Frequent disputes between providers and insurers highlight the importance of maintaining detailed records of all hospital documents, prescriptions, and test results to navigate potential issues effectively.

Claim Submission

The initial step in receiving reimbursement is the healthcare provider’s claim submission to your insurance carrier. This detailed form meticulously outlines the services you received, including specific diagnoses coded using ICD-10, and the procedures performed, identified by CPT codes.

Providers can submit claims electronically or via paper, though electronic submission is increasingly common for faster processing. The claim includes the provider’s charges, which are then subject to review by the insurer. Maintaining accurate patient information and ensuring the provider has current insurance details are vital for a smooth claim submission process, minimizing potential delays or denials.

Explanation of Benefits (EOB)

Following claim submission, you’ll receive an Explanation of Benefits (EOB) from your insurer – this is not a bill. The EOB is a detailed statement outlining how your claim was processed, including the charges submitted, the amount approved, any discounts applied, and your responsibility.

It clarifies what portion of the costs your insurance covered and what remains your out-of-pocket expense. Carefully reviewing your EOB is crucial to ensure accuracy and identify any discrepancies between the billed charges and the approved amount. Frequent disputes between hospitals and insurers necessitate diligent policyholder review.

Medical Coding (ICD-10 & CPT)

Accurate medical coding is fundamental to the health insurance billing process, utilizing standardized codes for diagnoses and procedures. ICD-10 codes classify diagnoses and reasons for healthcare encounters, while CPT codes detail the medical, surgical, and diagnostic services provided.

These codes translate medical services into a format insurers understand for claim processing. Errors or inconsistencies in coding can lead to claim denials or incorrect reimbursement. Healthcare providers employ trained coders to ensure precise code assignment, impacting both the provider’s revenue and your out-of-pocket costs.

Understanding Reimbursement

Reimbursement signifies the payment an insurer provides for covered healthcare services, but rarely matches the billed amount exactly. The “allowed amount” or “approved amount” is the maximum the insurer will pay, negotiated with providers. Your responsibility lies in understanding your out-of-pocket costs, including deductibles, copayments, and coinsurance.

These costs depend on your plan and the service received. Frequent disputes between hospitals and insurers highlight the need for policyholders to carefully review their Explanation of Benefits (EOB) statements, ensuring accurate billing and appropriate reimbursement. Knowing these factors helps manage healthcare expenses effectively.

Allowed Amount/Approved Amount

The allowed amount, also known as the approved amount, represents the maximum sum your health insurance plan will reimburse a healthcare provider for a specific service. This isn’t necessarily the actual charge, but a negotiated rate between the insurer and the provider. Understanding this is crucial, as you’re responsible for any difference between the allowed amount and the provider’s billed charge if you see an out-of-network provider.

Essentially, it’s the benchmark for reimbursement, impacting your out-of-pocket expenses. Always confirm the allowed amount before receiving non-emergency care to avoid unexpected costs.

Out-of-Pocket Costs

Out-of-pocket costs encompass expenses you’re responsible for, even with health insurance. These include deductibles, copayments, and coinsurance, and can significantly impact your healthcare spending. Rising premiums and these costs are a major concern for many, highlighting the need for careful plan selection.

Understanding your plan’s specifics is vital; knowing your deductible amount, copayment structure, and coinsurance percentage allows you to budget effectively. Frequent disputes between hospitals and insurers emphasize the importance of maintaining detailed records of all medical bills and receipts to manage these costs;

Navigating Claim Disputes

Disputes with insurance claims are unfortunately common, often stemming from disagreements over coverage or billing errors. Frequent tussles between hospitals and insurers necessitate proactive policyholders. The first step is thoroughly reviewing your Explanation of Benefits (EOB) and comparing it to your medical bills, identifying any discrepancies.

If issues arise, contact your insurance provider directly to understand the reason for the denial or reduced payment. Maintain detailed records of all communication, including dates, names, and summaries of conversations. If the initial appeal is unsuccessful, explore further appeal options as outlined in your policy documents, potentially seeking external review.

Health Reimbursement Arrangements (HRAs)

Health Reimbursement Arrangements (HRAs) are employer-funded health benefits that reimburse employees for qualified medical expenses. Unlike traditional insurance, HRAs don’t involve premiums; instead, employers allocate funds for employees to use. These funds can cover deductibles, copayments, and other out-of-pocket healthcare costs.

HRAs offer employers control over healthcare spending and provide employees with greater flexibility. Different types of HRAs exist, including Individual Coverage HRAs (ICHRA) and Qualified Small Employer HRAs (QSEHRA), each with specific eligibility requirements. Understanding the benefits and types of HRAs is crucial, especially when comparing them to Flexible Spending Accounts (FSAs).

Flexible Spending Accounts (FSAs)

Flexible Spending Accounts (FSAs) are employer-sponsored accounts that allow employees to set aside pre-tax money for eligible healthcare expenses. This pre-tax contribution lowers taxable income, resulting in significant savings. Funds in an FSA can be used for medical, dental, and vision care costs, including copayments, deductibles, and prescriptions.

FSAs typically operate on a “use-it-or-lose-it” basis, meaning any unused funds at the end of the plan year are forfeited, though some plans offer a grace period or limited carryover. Comparing FSAs to Health Reimbursement Arrangements (HRAs) is important, as HRAs are employer-funded, while FSAs are employee-funded through payroll deductions.

Coordination of Benefits (COB) ౼ Multiple Policies

Coordination of Benefits (COB) comes into play when an individual is covered by more than one health insurance plan, a situation increasingly common today. This process determines which plan pays first and how expenses are shared between insurers, preventing double payment. Typically, the plan that covers the insured as a primary member pays first, followed by the secondary plan;

Common scenarios include having coverage through an employer and a spouse’s plan, or possessing both individual and group insurance. COB rules are complex and vary, requiring careful attention to avoid claim denials and ensure proper reimbursement. Accurate record-keeping of all policies is crucial for a smooth COB process.

Record Keeping for Health Insurance Claims

Maintaining meticulous records is paramount when navigating health insurance claims, especially given frequent disputes between hospitals and insurers. Policyholders should diligently preserve all documentation related to healthcare services received. This includes hospital bills, doctor prescriptions, pharmacy receipts, and detailed test reports.

Organizing these documents – both physical copies and digital scans – facilitates claim submission and dispute resolution. Keeping a log of claim numbers, dates of service, and amounts paid is also highly recommended. Proactive record-keeping empowers individuals to effectively manage their healthcare finances and advocate for accurate claim processing.

Appealing Insurance Denials

Facing a denied claim doesn’t signify the end of the road; appealing the decision is a crucial right for policyholders. The initial step involves understanding the reason for denial, typically outlined in the Explanation of Benefits (EOB). Carefully review your policy details to ascertain coverage eligibility for the service in question.

Submit a formal written appeal to your insurance provider, including supporting documentation like medical records and a letter from your physician. If the internal appeal is unsuccessful, explore external review options offered by your state’s insurance department. Persistence and thorough documentation are key to a successful appeal.

The Role of Third-Party Administrators (TPAs)

Third-Party Administrators (TPAs) function as intermediaries between insurance companies, employers, and healthcare providers, streamlining the complex billing and reimbursement processes. They manage claims processing, negotiate provider rates, and handle member inquiries, relieving insurers of administrative burdens.

TPAs don’t assume insurance risk; instead, they administer plans on behalf of self-insured employers or insurance carriers. Frequent disputes between hospitals and insurers highlight the TPA’s role in resolving discrepancies and ensuring accurate claim settlements. Understanding their function is vital when navigating potential billing issues and appealing claim denials.

Preventive Care and Coverage

Most health insurance plans now prioritize and fully cover a range of preventive services, recognizing their long-term cost-effectiveness and health benefits. This includes routine check-ups, vaccinations, screenings for common conditions, and wellness programs, often without requiring copayments or deductibles.

However, coverage specifics vary significantly between plans. As healthcare costs continue to rise, focusing on preventive measures becomes increasingly important. Understanding what your plan covers can empower you to proactively manage your health and potentially avoid more expensive treatments down the line, ultimately impacting billing and reimbursement.

Rising Healthcare Costs and Insurance

The escalating cost of healthcare significantly impacts health insurance premiums, deductibles, and out-of-pocket expenses, creating financial strain for many individuals and families. Employer-sponsored plans are increasingly challenged, prompting exploration of alternative coverage options like Health Reimbursement Arrangements (HRAs) to address affordability.

These rising costs necessitate a thorough understanding of your insurance plan’s details, including allowed amounts and potential cost-sharing responsibilities. Proactive management of healthcare spending, coupled with awareness of available resources, is crucial for navigating the complex billing and reimbursement landscape effectively, and mitigating financial burdens.

Leave a Reply